Why Most People Get Journal Entries Wrong (And How to Fix It)

Your journal entries accounting process is broken, and you probably don't even realize it. These seemingly routine records actually control every financial statement your business produces. The Public Accounting Compliance Oversight Board identifies inaccurate journal entries as a leading cause of financial misstatements. When entries go wrong, your financial statements become "a complete mess".

Here's the reality: most organizations handle thousands of journal entries each month, turning what should be systematic into something tedious and error-prone. Every financial report your stakeholders see depends entirely on the accuracy of these foundational entries. Get them wrong, and your company suddenly looks more or less profitable than it actually is—affecting everything from tax obligations to compliance reporting.

The businesses that master journal entries gain something powerful: accurate tracking of transactions, reliable cash flow management, and real visibility into performance. Those that don't face a cascade of problems that start small but grow into major financial headaches.

You're about to discover exactly why journal entry mistakes happen so frequently and the specific steps to eliminate them from your business. Most importantly, you'll learn how to spot these issues before they distort the financial picture your team relies on for critical decisions.

Why Journal Entries Matter More Than You Think

Your journal entries control far more than most business owners realize. These records don't just document transactions—they shape every decision your stakeholders make about your company's future.

The role of journal entries in financial reporting

Every financial statement your organization produces starts with journal entries. Without proper entries, financial statements become meaningless and misleading. These records create the foundation that answers critical questions about your company's financial position.

Financial reporting translates your business activities into language that stakeholders understand. Journal entries create an essential audit trail, showing exactly what happened and when. This becomes invaluable when tracking down discrepancies months or years later.

Each journal entry maintains the fundamental accounting equation—Assets = Liabilities + Equity—in perfect balance. This systematic approach ensures your financial records actually reflect reality rather than wishful thinking.

How errors can impact business decisions

Small mistakes in journal entries create big problems for business operations. Even minor errors can trigger significant misstatements in financial reports, damaging compliance and stakeholder confidence.

Here's exactly what happens when your underlying accounting data is wrong: everyone who relies on it makes misinformed decisions. The ripple effects include:

- Managers making poor operating decisions based on inaccurate reports—especially dangerous when profit margins are tight

- External lenders approving or denying loans based on misleading financial statements

- Suppliers and customers questioning your reliability when transactions are handled incorrectly

Businesses with inaccurate journal entries often appear to have more or less debt, or seem more or less profitable than they actually are. This distorted view creates decisions based on false information, generating a cascade of negative consequences.

Accounting errors also drain productivity, making your staff less efficient while increasing labor costs. Companies that maintain clean journal entries consistently make better financial decisions because their data actually reflects what's happening in the business.

Why accuracy is critical for audits and compliance

Accurate journal entries provide complete documentation of all revenue, expenses, assets, and liabilities for auditing purposes. During audits, these entries prove that your financial statements fairly represent your business activities.

The Public Accounting Compliance Oversight Board notes that many audit deficiencies relate directly to journal entry examination. Auditors specifically scrutinize entries made to unusual accounts, entries created by people who don't typically make them, and those recorded at period-end with minimal explanation.

Beyond audits, journal entries maintain compliance with accounting standards such as GAAP or IFRS, ensuring consistency and transparency in financial reporting. Properly documented entries help prevent errors and fraudulent activities by capturing each transaction accurately, allowing quick identification and correction of discrepancies.

Investing time in proper journal entry procedures protects your business from regulatory penalties, audit failures, and the reputation damage that comes with financial misstatements. This isn't just bookkeeping—it's business protection.

What Are Journal Entries in Accounting?

Here's exactly what you need to know about the foundation of your entire accounting system. A journal entry is a detailed record of any financial transaction that affects at least two accounts. These entries function as the first step in double-entry bookkeeping, serving as your primary tool to document business financial activities in chronological order.

Every financial movement in your business gets captured through these entries—from purchasing office supplies to recording sales revenue. The core purposes include:

- Maintaining accurate financial records by tracking every transaction

- Ensuring transparency in financial reporting

- Complying with accounting standards and regulations

- Providing the foundation for all financial statements

- Simplifying audits and strengthening financial accountability

Journal entries offer a structured method to document financial transactions with the clarity and precision your business needs.

Understanding the double-entry system

The double-entry accounting system records business transactions where every financial event creates equal and opposite effects in at least two different accounts. The fundamental principle is straightforward: for every debit, there must be an equal and corresponding credit.

This system ensures the accounting equation—Assets = Liabilities + Equity—stays balanced at all times. Since a debit in one account offsets a credit in another, total debits must always equal total credits.

Beyond standardizing your accounting process, this systematic approach improves the accuracy of financial statements. Any imbalance immediately signals a problem in your records, allowing you to catch errors before they multiply.

Key components: date, accounts, amounts, description

Every properly formatted journal entry requires specific elements:

- Transaction Date: Records exactly when the financial transaction occurred

- Accounts Affected: Identifies the specific accounts being debited and credited

- Debit and Credit Amounts: Shows the monetary values assigned to each account

- Description or Narration: Provides a brief explanation of the transaction's purpose

- Reference Number (Optional): Includes a unique identifier for tracking the entry

The transaction date maintains chronological order in your books while ensuring accurate record-keeping. Knowing which accounts are affected is crucial since each transaction impacts at least two accounts.

Debit and credit amounts must always be equal to maintain balance in your books. Clear descriptions provide context that becomes invaluable when reviewing entries months or years later.

Master these core components, and you'll create accurate journal entries that properly document business transactions, leading to reliable financial statements and better business decisions.

The 6 Most Common Mistakes People Make

Most businesses make the same journal entry mistakes repeatedly, and these errors follow predictable patterns. After seeing these issues across countless organizations, here's exactly what goes wrong and how to fix each problem before it damages your financial reporting.

1. Misclassifying accounts

Account misclassification happens when transactions land in the wrong category—treating an asset as an expense or recording revenue as a liability. These classification errors create incorrect accounting entries that significantly distort your financial position. The damage compounds when misclassifications cross between balance sheet and income statement categories, affecting retained earnings calculations and beginning year balances.

Misclassified accounts are also potentially handled incorrectly at year-end, with balances either incorrectly zeroed out to retained earnings or inappropriately accumulating into the next year. The fix: establish clear account coding guidelines and require secondary review for any non-routine classifications.

2. Forgetting to record transactions

Omission errors occur when financial transactions never make it into your books. This mistake happens most frequently when business owners juggle multiple responsibilities and lose track of smaller transactions.

Common forgotten items include minor expenses, petty cash disbursements, inventory adjustments, or even revenue. These omissions cause your balance sheet to present an inaccurate financial picture. Set up systematic transaction capture processes—daily entry schedules, receipt collection systems, and regular account reviews catch these oversights before they accumulate.

3. Imbalanced debits and credits

Unbalanced entries break the fundamental rule of double-entry bookkeeping. Each journal entry needs equal debits and credits. These imbalances typically result from:

- Manual edits that change amounts without maintaining balance

- System errors in auto-populated information

- Simple calculation mistakes when determining entry amounts

Most accounting systems flag these errors automatically. However, manual review processes help identify balance issues before they create reporting problems.

4. Using vague descriptions

Poor transaction descriptions create internal control problems and complicate audits. Every journal entry requires clear explanations: a header describing the overall purpose and specific line descriptions for each component. Without adequate detail, reviewers cannot verify transaction accuracy or reasonableness.

Generic descriptions like "adjustment" or "correction" provide insufficient context and make future reviews nearly impossible. Include specific business justification for each entry—the extra detail saves hours during month-end reviews and audit preparation.

5. Skipping adjusting entries

Missing adjusting entries produces inaccurate financial statements. These oversights cause:

- Overstated or understated profits

- Incorrect tax reporting

- Difficulty obtaining financing due to unreliable statements

Commonly missed adjustments include unbilled revenue, accrued expenses like utilities or wages, depreciation on fixed assets, and prepaid items such as insurance or rent. Build month-end checklists that systematically address each adjustment category.

6. Not reconciling regularly

Regular reconciliation ensures actual money movement matches recorded account activity. Without consistent reconciliation, errors compound and become increasingly difficult to trace and correct.

Account reconciliation identifies irregularities including incorrect amounts, duplicate entries, and data entry errors. Regular reconciliation also helps detect potential fraud before significant damage occurs. Monthly reconciliation represents the minimum frequency—high-volume accounts may require weekly or even daily attention to maintain accuracy.

Journal Entries Accounting Examples That Clarify Everything

Here's exactly what proper journal entries look like in practice. These four examples show you how to handle the most common situations your business faces every day.

Simple journal entry example

Most transactions follow this straightforward pattern—one debit, one credit. When a company receives $2,000 cash for services rendered:

Notice how the cash increase matches exactly with the revenue increase. This maintains the fundamental balance while clearly documenting what happened.

Compound journal entry example

Real business transactions often affect multiple accounts simultaneously. Compound entries handle these complex situations efficiently. Take purchasing raw materials with delivery charges:

This single entry captures the entire transaction instead of creating separate records for materials and delivery costs.

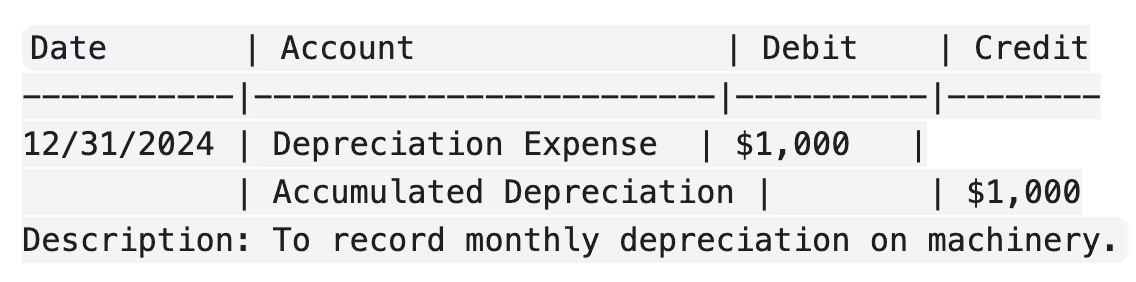

Adjusting entry example

Month-end adjustments ensure your financial statements reflect actual business activity, not just cash movements. Equipment depreciation provides a classic example:

This entry properly matches equipment costs with the periods that benefit from using the equipment.

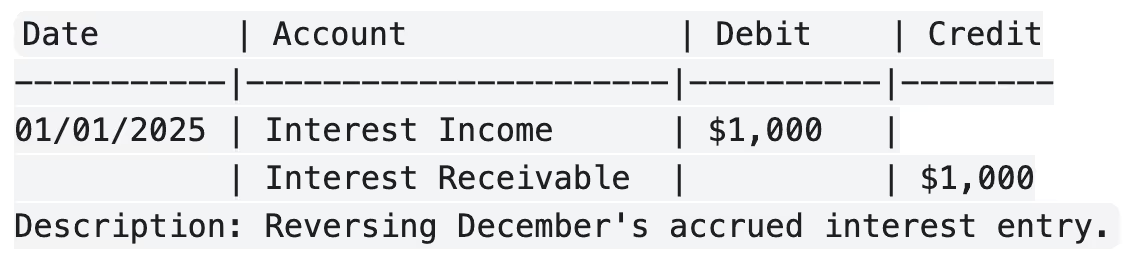

Reversing entry example

Some adjustments need to be "undone" at the start of the next period to prevent double-counting. Reversing entries handle this automatically. For $1,000 interest income accrued in December:

This reversal clears the slate so when the actual interest payment arrives, you can record it normally without creating duplicate income.

How to Fix Your Journal Entry Process

Your journal entry problems won't fix themselves with occasional patches. What you need is a systematic overhaul of how these critical records get created, reviewed, and posted. The businesses that get this right see dramatic error reduction while freeing up valuable staff time.

Use templates for recurring entries

Stop recreating the same journal entries from scratch every month. Standardized templates for frequently used entries eliminate guesswork and ensure consistency. These templates contain complete account information for identical transactions that repeat across multiple periods, preventing your accountants from accidentally posting to wrong accounts.

Automate routine transactions

Manual journal entry processing is eating up roughly 30% of your accounting team's day. Top-performing organizations have figured this out—they automate 58% of their journal line items. Modern automation uses optical character recognition and machine learning to extract data automatically, handling the time-consuming work that keeps your team from higher-value activities.

Set up a clear approval workflow

Every journal entry should pass through structured approval before hitting your books. Automated workflows establish routing rules based on your criteria—dollar thresholds, account types, or transaction complexity. This approach enforces consistent procedures while creating detailed audit trails that satisfy both internal controls and external auditors.

Attach supporting documents

Each journal entry needs documentation that proves its accuracy and supports the amounts recorded. These attachments should validate both the dollar amounts and the account classifications you're using. Make sure all supporting documents are available when entries go through your approval process.

Reconcile frequently

Monthly reconciliation catches problems while they're still manageable. This process verifies that actual cash movements match what's recorded in your accounts. Regular reconciliation identifies issues early and can detect potential fraud before significant damage occurs. Without this routine check, small errors compound into major headaches.

Conclusion

Your journal entry accuracy directly determines whether your financial statements tell the truth about your business or mislead everyone who depends on them. The six critical mistakes we've covered—misclassifying accounts, forgotten transactions, unbalanced entries, vague descriptions, missed adjustments, and irregular reconciliation—represent the most common ways businesses unknowingly distort their financial picture.

Here's exactly what you need to know: these aren't just bookkeeping problems. They're business decision problems. When your underlying data is wrong, every choice your team makes becomes a gamble based on false information.

The solutions work because they address root causes rather than symptoms. Templates eliminate guesswork from recurring entries. Automation removes human error from routine tasks. Clear approval workflows catch problems before they reach your financial statements. Supporting documentation provides the audit trail you need. Regular reconciliation spots discrepancies while they're still manageable.

Working with businesses over the years, the pattern is clear: companies with clean journal entry processes make better financial decisions because their data actually reflects reality. Those with sloppy processes constantly react to problems they can't see coming.

Your next move should be systematic. Pick one solution and implement it fully before moving to the next. Start with the area causing you the most pain right now. Most businesses see immediate improvement once they tackle their biggest journal entry weakness.

Clean journal entries don't just keep auditors happy—they give you the financial clarity needed to grow your business confidently. The time you invest in fixing these processes pays back through better decisions, fewer surprises, and stakeholders who trust your numbers.

The businesses that get this right gain a competitive advantage: they know their true financial position while their competitors operate on guesswork.

If you want cleaner journal entries and a month-end you can trust, we can help standardize templates, automate recurring entries, and tighten approvals and reconciliations. Book a quick intro with our team here — or start with a free Financial Fitness Score here to see where your process stands.

Ready to Get Started with AdaptCFO?

We provide the tools to become more skilled at financial literacy. Learn more about our different service levels.

View Pricing