Why Most People Get Journal Entries Wrong (And How to Fix It)

Journal entry mistakes are quietly sabotaging businesses every single day. You might think recording a simple debit and credit is straightforward, but I've seen companies make the same critical errors repeatedly—errors that ripple through every financial report they produce.

Here's the reality: when you mess up journal entries, you're not just making a small bookkeeping mistake. You're creating unreliable financial data that leads to poor decisions about everything from cash flow to growth investments. The double-entry system requires that every transaction affects two accounts—one debited, one credited—and these amounts must balance perfectly. Miss this basic requirement, and your entire accounting system becomes questionable.

A proper journal entry needs four essential components: the correct date, accurate amounts, a clear description of what happened, and a unique reference number for tracking. Sounds simple enough, right? Yet businesses consistently struggle with these basics, creating unbalanced entries where debits don't equal credits.

The pattern is predictable: poor journal entries lead to unreliable financial statements, which lead to business decisions based on bad information. This article shows you exactly how to identify the most common journal entry mistakes and gives you straightforward methods to fix them before they damage your financial reporting.

What is a Journal Entry and Why It Matters

Think of journal entries as the DNA of your accounting system—they contain all the essential information that gets replicated throughout your financial reports.

Definition of a journal entry

A journal entry is simply a formal way to record what happened in your business financially. Every entry needs five basic pieces:

- The date when the transaction occurred

- The specific accounts affected by the transaction

- Debit and credit amounts for each account

- A brief but clear description of the transaction

- A unique reference number for tracking purposes

The magic happens through double-entry accounting. Every transaction touches at least two accounts—one gets debited, another gets credited—and these amounts must always equal each other. This keeps the fundamental accounting equation (Assets = Liabilities + Equity) balanced after every single transaction.

Take purchasing $1,000 of office supplies on credit. You'd debit Office Supplies (increasing your assets) and credit Accounts Payable (increasing what you owe) for the same amount. The entry balances perfectly.

Why journal entries are the foundation of accounting

Without proper journal entries, financial statements become meaningless. These records create the foundation for everything else in your accounting system.

Journal entries serve as your audit trail, showing exactly what happened and when it happened. This becomes critical during audits or when you need to track down discrepancies months later. The double-entry system acts as a built-in error detector—when debits don't equal credits, you know immediately that something's wrong.

Every financial statement your business produces—balance sheets, income statements, cash flow statements—depends entirely on accurate journal entries. Bad entries create bad reports, which lead to bad business decisions.

From experience working with businesses over the years, companies that maintain clean journal entries consistently make better financial decisions. The data they're working with actually reflects reality.

How journal entries connect to the general ledger

Journal entries record transactions chronologically, but the general ledger organizes this same information by account type.

The connection happens through "posting"—transferring information from journal entries into specific accounts in the general ledger. When you record a $500 cash sale, posting ensures this amount appears in both your Cash account and Sales Revenue account in the general ledger.

This creates a clear information flow: Transaction → Journal Entry → General Ledger → Financial Statements

Each step builds on the previous one. Accurate journal entries create reliable general ledger balances, which produce trustworthy financial statements. Start with solid entries, and everything downstream stays accurate.

The Most Common Mistakes People Make

These five journal entry errors show up repeatedly across businesses of all sizes. Each mistake might seem minor on its own, but together they create serious problems that distort your financial picture and lead to poor decisions.

1. Confusing debits and credits

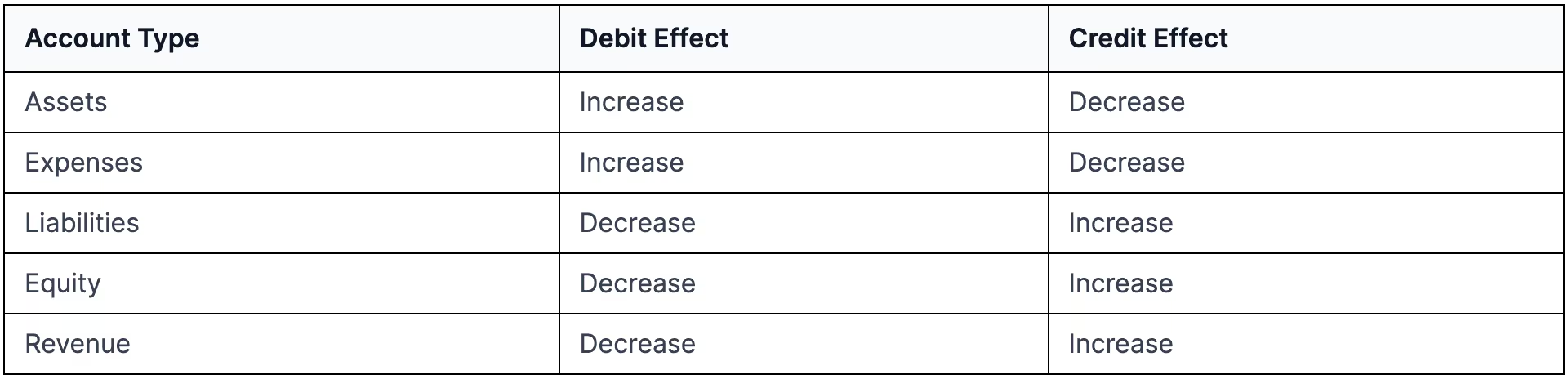

Debits and credits function differently depending on which type of account you're working with. Assets and expenses increase with debits and decrease with credits. Liabilities, equity, and revenue accounts work the opposite way—they increase with credits and decrease with debits.

This reversal catches even experienced bookkeepers off guard. The fundamental rule stays constant: debits must always equal credits in every journal entry. When this balance breaks, your books become unreliable, and your financial statements stop reflecting reality.

2. Using the wrong account types

Account misclassification happens when transactions get recorded in the wrong category. Put an asset in an expense account, or record a liability as revenue, and you've distorted your financial position significantly.

These classification errors create incorrect accounting entries that make financial statements inaccurate. The damage multiplies when misclassifications cross between balance sheet and income statement categories, affecting retained earnings calculations and beginning year balances.

3. Missing or vague descriptions

Poor descriptions create internal control problems and audit headaches. Every journal entry needs two types of descriptions: a header that explains the overall purpose and individual line descriptions for each transaction component.

Without clear explanations, approvers can't verify that transactions are reasonable and accurate, potentially causing audit failures. Entries become particularly problematic when the business justification can't be determined from the description alone.

4. Not balancing the entry

Unbalanced entries violate the most basic rule of double-entry bookkeeping. Each journal entry requires at least one debit and one credit, with total values matching exactly. Most accounting systems flag these errors and prevent posting until you fix the imbalance.

Common causes include:

- Manual edits that change amounts without maintaining balance

- System errors in auto-populated information

- Simple math mistakes when calculating entry amounts

5. Posting to the wrong period

Timing errors occur when transactions get recorded in the wrong accounting period. These mistakes break the matching principle—expenses should be reported in the same period as the revenues they helped generate.

Wrong-period posting artificially inflates or deflates results for specific timeframes. This particularly impacts financial statements crossing fiscal years, potentially affecting tax liabilities and misleading stakeholders about business performance.

Here's exactly what you need to know: these accounting errors might look small individually, but collectively they significantly distort financial reporting. Understanding these common patterns gives you the knowledge to implement preventative measures and maintain accurate books that properly reflect your business reality.

Understanding Debits and Credits the Right Way

Debits and credits don't have to be confusing. The problem isn't that these concepts are inherently difficult—it's that most people learn them backwards, focusing on mechanical rules instead of understanding the logic behind double-entry bookkeeping.

How debits and credits affect different account types

Here's exactly what you need to know: debits and credits aren't "good" or "bad" entries. They're simply the left side and right side of an account. The confusion comes from their opposite effects depending on which type of account you're working with:

Use this memory trick: D-E-A-L (Dividends, Expenses, Assets, Losses) accounts increase with debits, while G-I-R-L-S (Gains, Income, Revenue, Liabilities, Stockholders' equity) accounts increase with credits.

The accounting equation explained

Every journal entry must respect the fundamental accounting equation: Assets = Liabilities + Equity. This isn't just an academic concept—it's the mathematical foundation that keeps your books balanced.

When you record any transaction, total debits must always equal total credits. This balance isn't optional; it's built-in verification that your financial position remains accurate after every entry.

Take a simple example: your company receives a $10,000 loan. Assets (cash) increase by $10,000, and liabilities (loans payable) increase by the same amount. The equation stays perfectly balanced, confirming your entry is correct.

Journal entry example: asset vs. liability

Let's work through a real scenario. Your business buys $16,000 of equipment, paying half in cash and financing the remainder:

Notice how total debits ($16,000) equal total credits ($8,000 + $8,000). The equipment asset increases with a debit, cash decreases with a credit, and the new liability increases with a credit.

Stop thinking of debits and credits as additions or subtractions. Instead, focus on how they affect specific account types. Once you understand these patterns, journal entries become straightforward rather than mysterious.

Fixing Journal Entry Errors: Step-by-Step

Finding mistakes in your books isn't the end of the world—it's an opportunity to strengthen your accounting processes. Here's exactly what you need to know to clean up journal entry errors quickly and prevent them from happening again.

1. Identify the incorrect entry

Start with your trial balance. When debits don't equal credits, you've got a problem that needs immediate attention. Look for these red flags:

- Account balances that seem unusually high or low

- Transactions that don't match your bank statements

- Missing entries for known business activities

- Amounts that don't align with supporting documentation

Check your financial statements monthly—income statement, balance sheet, and cash flow. Catching errors early saves you from bigger headaches later. Pay particular attention to transaction dates and make sure expenses are recorded in the right accounting periods.

2. Reverse or adjust the entry

You have two ways to fix journal entry mistakes, and the method depends on your situation:

Adjustment Method - Calculate the difference between what you recorded and what should have been recorded. Create an entry for just the difference.

Reversal Method - Create an entry that exactly reverses the wrong entry, then record a completely new, correct entry.

Say you collected $200 from a customer but only recorded $150. An adjustment entry would debit cash and credit accounts receivable for the $50 difference.

3. Repost with correct details

When you create the corrected entry, double-check these critical elements:

- Right accounts and account classifications

- Balanced debits and credits

- Correct transaction date (not necessarily today's date)

- Clear description explaining what happened and why you're correcting it

Before you finalize anything, make sure your correction doesn't mess up your current month's reporting or create weird trends in your financial analysis.

4. Use a journal entry template for consistency

Templates prevent most journal entry mistakes before they happen. They create a consistent structure that reduces errors and speeds up your accounting workflow.

Templates give you "a track to run on"—especially helpful when you're busy or distracted. Instead of reinventing your process every time, you can focus on accuracy and gradually improve your methods.

Examples of Correct Journal Entries

Journal entries become clearer when you see them applied to actual business situations. These examples show proper structure and balance across different accounting scenarios.

General journal entries examples

Daily business transactions form the core of general journal entries. When a client pays a $600 invoice, the entry looks like this:

Office supply purchases follow the same principle—debit Office Supplies for $100, credit Cash for $100. The balance remains intact while accurately recording the transaction.

Adjusting entry example

Period-end adjusting entries capture expenses that occurred but haven't been recorded yet. Monthly depreciation provides a common example:

Notice how this recognizes asset usage costs without any cash changing hands during the period.

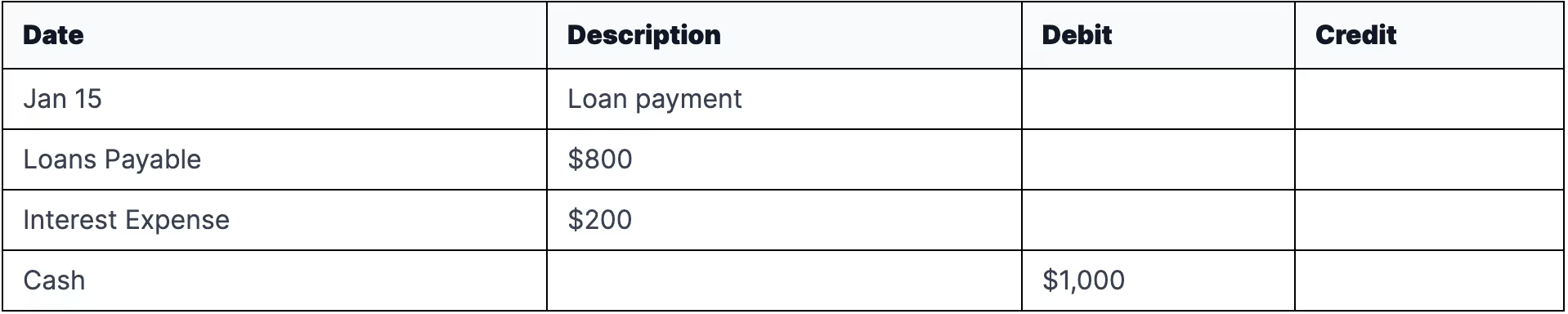

Compound entry example

Some transactions affect more than two accounts. A loan payment of $1,000 splits between $800 principal and $200 interest:

The total debits still equal the credit amount—$1,000 each side—while properly allocating the payment between debt reduction and interest cost.

Reversing entry example

Reversing entries simplify certain accrual situations. After accruing $1,000 interest income on December 31, 2021, the January 1, 2022 reversal looks like this:

This technique prevents double-counting when the actual payment arrives later.

Conclusion

Journal entries look simple on the surface, but they are the foundations of your accounting system. Many professionals find it challenging to grasp the basic concepts of debits and credits. Your financial records will stay accurate and reliable once you become skilled at these principles. Your financial picture can become substantially distorted by common mistakes we discussed - mixing up debits with credits, using wrong account types, writing vague descriptions, making unbalanced entries, and posting to incorrect periods.

What seems complex at first becomes a logical, systematic process as you learn how debits and credits work in different account types. Assets and expenses increase with debits, while liabilities, equity, and revenue accounts increase with credits. This knowledge combined with the accounting equation helps you keep balanced books that show your business's true picture.

A methodical approach to finding and fixing errors stops small mistakes from becoming major financial misstatements. Your best defense against recurring journal entry problems comes from using standardized templates and consistent review practices.

This piece shows examples of properly structured entries for scenarios of all types. You can build strong financial reporting foundations that support good business decisions by doing this and avoiding these pitfalls. Need advice about your finances? Book a call with our team here, or get your free Financial Fitness Score here.

Journal entries are just one part of accounting, but their accuracy determines how reliable all later financial analysis will be. Your attention to detail at this basic level rewards you with trustworthy financial statements that guide your business toward growth and profitability.

Ready to Get Started with AdaptCFO?

We provide the tools to become more skilled at financial literacy. Learn more about our different service levels.

View Pricing