How Fixed Assets Quietly Make—or Break—Your Business

Your business operations rely heavily on fixed assets - those long-term tangible properties you can't easily convert to cash. The balance sheet lists buildings, machinery, vehicles, and equipment as property, plant, and equipment (PP&E). These valuable resources help your business in many ways, from running operations and production to renting them out to others.

Fixed assets are physical or tangible assets that your company owns and uses daily to serve customers and generate income. Your business needs to hold and use these assets for at least a year to qualify them as fixed assets. These assets lose value over time through depreciation, except for land. Fixed assets matter not just because they cost a lot, but also because their accounting treatment can benefit your company. The more fixed assets a company owns, the more attractive it becomes to potential investors and buyers looking for mergers and acquisitions.

This piece will give you everything you need to know about managing these crucial business assets. You'll learn about their key features, various types, accounting methods, and how they affect financial statements. We'll also share practical ways to get the most value from your long-term business assets.

Fixed Assets Definition and Key Characteristics

Your business's fixed assets need a solid accounting framework based on their core features. These resources serve as vital elements in your company's operations.

What are fixed assets in accounting?

Fixed assets are long-term tangible properties your business owns and uses to generate revenue. You'll find these physical resources listed on your balance sheet as property, plant, and equipment (PP&E). They help create, house, and ship your finished goods, unlike inventory meant for sale.

Your business uses fixed assets for:

- Production of goods or services

- Office and operational use

- Rental to third parties

Buying a fixed asset doesn't count as an expense. Your business capitalizes it on the balance sheet as a long-term asset. The asset's value then decreases over time through depreciation methods that show its declining worth during its useful life.

Tangible vs intangible fixed assets

The main difference between tangible and intangible fixed assets shows up in their physical presence and how we value them. Buildings, machinery, vehicles, and equipment are tangible fixed assets. You can see and touch these resources, and they wear down over time.

Intangible fixed assets don't have physical form but add long-term value through legal protections and brand reputation. Patents, trademarks, and copyrights are good examples. These assets usually go through amortization instead of depreciation, though both methods spread costs over the asset's useful life.

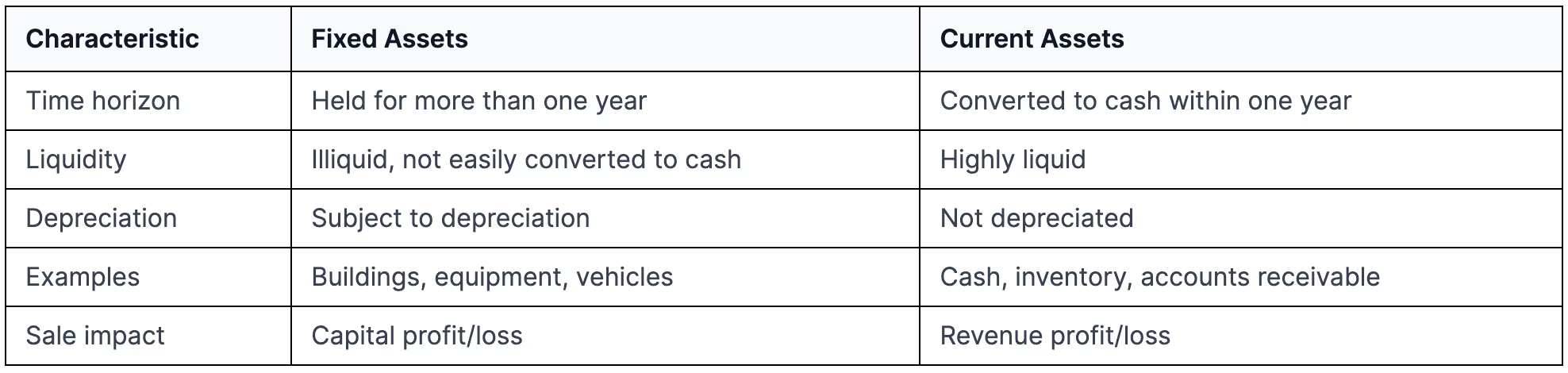

Fixed assets vs current assets: Key differences

Here's how fixed assets stand apart from current assets:

Your business can't quickly turn fixed assets into cash for day-to-day expenses. During tough economic times, current assets help generate quick cash, while fixed assets need more time to sell without losing much value.

Useful life and illiquidity explained

An asset's useful life shows how long it can generate revenue affordably. This estimate helps determine the depreciation period, which usually spans several years. Usage patterns, age at purchase, and new technology all affect an asset's useful life.

Fixed assets lose value as they age, except for land. This calls for systematic cost allocation through depreciation. Your options for depreciation include:

- Straight-line: Equal annual amounts over the asset's life

- Declining balance: Higher depreciation early on, with smaller amounts later

Fixed assets are illiquid because selling them quickly leads to big value losses. Companies with mostly illiquid assets might struggle with cash flow during financial stress. This creates a basic business risk - even with millions in fixed assets, your company could face problems if it can't pay immediate bills.

Types and Examples of Fixed Assets by Industry

Fixed assets are big investments that businesses of all sizes need. Each business needs specific long-term assets that match their operations and help them make money.

Land, buildings, and leasehold improvements

Land stands out among fixed assets because you can't depreciate it - it lasts forever. Your balance sheet lists land as a fixed asset, and it's the hardest asset to convert to cash. Companies buy land with or without buildings to run their operations, not to resell it or speculate.

Buildings are a big deal as they mean that businesses must invest heavily in fixed assets. These include office spaces, manufacturing plants, storage warehouses, and retail stores. Buildings lose value over time, unlike land, and depreciate over 39 years. The cost includes everything from construction expenses to purchase price.

Leasehold improvements are changes and upgrades you make to property you rent. These improvements have:

- Built-in cabinets and interior walls

- Electrical and plumbing upgrades

- Office space modifications

- Air conditioning installations

- Telephone wiring

Accounting rules say you must spread leasehold improvement costs over their useful life or remaining lease term - whichever is shorter. But common control leases let you spread these costs over their useful life to the common control group, no matter the lease term.

Machinery, vehicles, and tools

Machinery covers equipment that helps employees work better. Manufacturing equipment, commercial printers, and construction tools fit here. These assets help production processes in businesses of all types.

Vehicles are vital fixed assets that many businesses need, especially transport companies, airlines, rental agencies, and shipping operations. Company cars, trucks, forklifts, and specialized moving equipment help both internal operations and customer service. IRS rules let you depreciate vehicles over five years.

Tools are another significant fixed asset, especially to production businesses that invest heavily in specialized equipment. Notwithstanding that, many companies set value limits below which they expense tools right away instead of treating them as capital assets.

Computer equipment and office furniture

Computer equipment covers hardware like PCs, laptops, servers, and tablets that run your daily operations. Most businesses need these, but whether they count as fixed assets depends on your company's value threshold. The total cost, including freight, taxes and installation, should exceed your threshold to count as a fixed asset.

Office furniture becomes a fixed asset when you plan to use it long-term. Desks, chairs, filing cabinets, lighting fixtures, and break room appliances are tangible fixed assets above your value threshold. These items usually lose value over 5-10 years through wear and becoming outdated.

Industry-specific classification: Inventory vs fixed asset

The difference between inventory and fixed assets comes down to purpose and timing. Fixed assets make money through regular use, while inventory is property you plan to sell within a year.

Your industry determines how you classify assets. To name just one example, see how tractor supply companies list tractors as inventory, but commercial farmers record them as fixed assets. Equipment that helps run your business counts as a fixed asset, while stationery items or consumables are inventory because they move quickly.

The financial side shows fixed assets on your balance sheet as non-current assets under property, plant and equipment. You record these at net book value - original cost minus total depreciation. Inventory appears as a current asset at purchase price since you expect to turn it into cash within a year.

Accounting for Fixed Assets Throughout Their Lifecycle

Meticulous tracking of fixed assets throughout their lifecycle demands proper accounting from acquisition to disposal. Each stage must follow specific accounting principles that accurately show the asset's value on financial statements.

Capitalization rules and initial recognition

Fixed assets qualify for capitalization when they provide future economic benefits and have measurable costs. Business assets must have a useful life beyond one year to qualify for capitalization. Most organizations set materiality thresholds—typically between $2,500 and $5,000. Purchases below these thresholds are expensed immediately rather than capitalized.

The original cost has all expenditures needed to prepare the asset: purchase price, transportation, installation, and professional fees. Constructed assets might include costs of materials, labor, overhead, and applicable interest expenses.

Straight-line vs declining balance depreciation

Straight-line depreciation makes calculations simple and reduces errors by allocating equal expense amounts over an asset's useful life. The formula remains: Annual Depreciation = (Cost - Salvage Value) ÷ Useful Life

Declining balance methods front-load depreciation expenses in early years. This approach better reflects how technology assets lose value through obsolescence. The calculation stays: Depreciation = Book Value × Depreciation Rate

Let's look at an example using double-declining balance (a rate twice that of straight-line). A $10,000 asset with 5-year life would have first-year depreciation of $4,000 compared to $2,000 using straight-line.

Impairment and revaluation of fixed assets

Assets need impairment testing when events suggest their carrying value might exceed recoverable amounts. Market value drops, operational changes, or physical damage often trigger this testing. The asset's value gets written down to fair value with immediate loss recognition if impairment exists.

Some accounting standards allow upward revaluation to reflect current market values. This adjustment increases both the asset's carrying amount and creates a revaluation reserve in equity.

Disposal and write-off procedures

Asset disposal through sale, scrapping, or donation requires complete removal from your balance sheet. The accounting process needs:

- Reversing accumulated depreciation

- Removing the original asset cost

- Recording any cash proceeds

- Recognizing gain or loss on disposal

Here's a practical example: Selling a $100,000 machine with $70,000 accumulated depreciation for $35,000 results in a $5,000 gain. Proper asset control requires written authorization before any disposal.

Impact of Fixed Assets on Financial Statements

Fixed assets substantially affect your financial statements and show how well you manage operations and investments. Their effects reach every major financial report and shape how stakeholders review your business performance.

Balance sheet: PP&E and net fixed assets

Property, Plant, and Equipment (PP&E) shows up as a non-current asset on your balance sheet. It represents much of the total assets for capital-intensive businesses. Net PP&E equals gross value plus capital expenditures minus accumulated depreciation. This formula captures new investments and the ongoing value reduction through depreciation. PP&E makes up the largest part of total assets for most companies, especially in manufacturing or industrial sectors.

Income statement: Depreciation expense

Your income statement shows depreciation expense that spreads fixed asset costs over their useful lives. This non-cash expense lowers reported net income but doesn't affect cash flow. A $500,000 machine with $100,000 salvage value after five years would create $80,000 in yearly depreciation. The operating expenses section records this expense when you use the asset for production.

Cash flow statement: Investing activities

Fixed asset transactions stand out in the investing activities section of your cash flow statement. Capital expenditures show cash outflows for fixed asset purchases and make up one of the biggest investing activities. Asset sales appear as cash inflows. These transactions reflect long-term business investments rather than daily operations and help stakeholders learn about your company's growth strategy.

Fixed asset turnover ratio calculation

The fixed asset turnover ratio shows how well you generate revenue from fixed asset investments using this formula:

Fixed Asset Turnover = Net Revenue ÷ Average Fixed Assets

Where Average Fixed Assets = (Beginning + Ending Fixed Assets) ÷ 2

A higher ratio points to better efficiency in using fixed assets to create sales. A ratio of 2.0 means each dollar of fixed assets brings in $2.00 in revenue. Optimal ratios vary between industries. Capital-intensive businesses usually have lower ratios than asset-light operations.

Managing Fixed Assets for Long-Term Business Value

Smart management of fixed assets can improve their value to your business's long-term success by a lot. Good oversight throughout the asset lifecycle helps you get maximum returns while keeping costs down.

Setting materiality thresholds for capitalization

The right capitalization thresholds help avoid the hassle of tracking many low-value items. The Government Finance Officers Association suggests minimum thresholds of at least $5,000 per item with a useful life over two years. A fixed capitalization amount ensures consistent accounting and makes it easier to spot errors. You can set different thresholds for various asset classes based on their importance to your business.

Tracking maintenance and repairs

Scheduled maintenance plays a key role in maximizing asset value. Expense tracking helps with budgeting and service history records support smart replacement decisions. Good maintenance programs extend asset life, cut down unexpected breakdowns, and reduce repair costs. Unexpected downtime can cost businesses up to $260,000 per hour. Asset tagging throughout their lifecycle prevents theft, stops misplacement, and helps with financial reporting.

Using fixed assets as loan collateral

Your company's major fixed assets can work as collateral through asset-based lending (ABL). This gives you needed capital without strict cash-flow rules. ABL offers more flexibility, especially for businesses that deal with seasonal changes or short-term cash flow issues. Companies rich in assets that need substantial capital despite changing cash flows make great candidates for ABL.

Avoiding underutilization and overinvestment

Underutilization and overinvestment hurt value and your firm's performance. Regular asset audits help find equipment that's not being used enough. Managers who invest in negative NPV projects often cause overinvestment, which can lead to business failure. Missing valuable opportunities creates underinvestment problems. You can improve utilization by moving underused assets to departments that need them more or by setting up maintenance programs based on actual usage instead of fixed schedules.

Conclusion

Fixed assets are the foundations of your business operations. These assets need strategic management throughout their lifecycle. Your long-term investments keep generating value and support daily operations through proper capitalization, tracking, and maintenance. The right accounting treatment of fixed assets helps you make smart decisions about acquisitions, disposals, and financial reporting.

The strength of your balance sheet depends on how well you manage property, plant, and equipment. Setting the right materiality thresholds, picking suitable depreciation methods, and doing regular impairment tests are key practices for financial accuracy. Fixed assets may be illiquid investments, but they offer collateral opportunities and add a high value to your company's overall worth.

The fixed asset turnover ratio is a key metric to review operational efficiency compared to industry standards. Your asset management strategy should focus on avoiding underutilization and overinvestment. Regular audits help find ways to move resources around, maintain equipment before it breaks, or get rid of assets that aren't performing well.

Fixed assets ended up being more than just accounting entries—they show your company's operational capabilities and growth potential. Good management means balancing current operational needs with future investment opportunities while keeping accurate financial records. Need advice on your finances? Book a call with our team here, or get your free Financial Fitness Score here.

Becoming skilled at fixed asset management takes time and expertise. In spite of that, the rewards make it worth the effort. You'll see increased efficiency, better financial reporting accuracy, stronger balance sheets, and in the end, greater business value. Your long-term success relies on turning these physical resources into strategic advantages that support steady growth.

Ready to Get Started with AdaptCFO?

We provide the tools to become more skilled at financial literacy. Learn more about our different service levels.

View Pricing